Investing in the stock market is a strategic decision that requires assessing different possibilities, such as choosing between blue-chip and mid-cap stocks in India. The National Institute of Wall Street (NIWS) is one of the stock market course in Jaipur, Delhi, and India. We teach people the skills they need to understand and manage the complicated financial markets.

We are committed to giving aspiring investors and traders the tools they need. Our experience spans over 15 years, and our curriculum includes modules from NSE, BSE, SEBI, NCFM, and NISM. In this article, we will look into the comparative analysis of investing in blue-chip stocks versus mid-cap stocks in India.

A blue-chip stock is issued by a big, well-known, financially stable company with a great image. These kinds of companies have usually been around for a long time, have steady profits, and pay investors dividends.

A blue-chip company usually has a market value in the billions. It's usually the market leader or one of the top three companies in its field, and most people have heard of it.

Because of these things, blue-chip stocks can be suitable investments and are some of the most popular stocks buyers buy. A few examples of blue-chip stocks are American Express, Microsoft, McDonald's, IBM Corp, and Boeing Co.

Here are some advantages of investing in blue-chip stocks:

Blue-chip stock buyers get stable returns on their investments regardless of market conditions. These kinds of profits come in the form of dividends, which are given to investors every three months.

As a long-term investment choice with a more than seven-year horizon, it gives investors much time to save money and build up a good nest egg over the years.

Blue-stock companies are high-profile businesses that don't profit from just one source. It helps them cover their losses when things go wrong with their operations and spreads out the risks of owning blue-stock shares.

Blue-chip enterprises have a strong market reputation and a high credit rating. It directly raises the market value of blue-chip stocks, making them a good choice for buyers. It also makes buying and selling these stocks easier, making them more liquid.

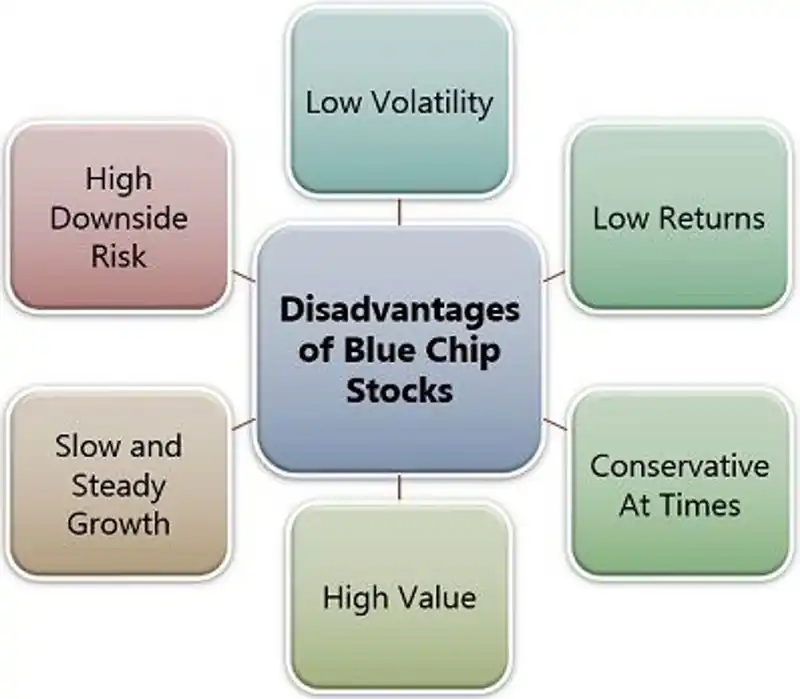

Here are some disadvantages of investing in blue-chip stocks:

Blue-chip stocks don't grow very fast, suggesting investors must be patient to receive the desired returns.

Blue chip stocks might not pay high dividends because their growth rate is slow.

People usually want blue-chip stocks because they are reliable, low-risk, and less volatile. As a result, they are more expensive in the market than other equities of equal size.

A rough term for companies and stocks in the middle of the large-cap and small-cap categories is "mid-cap."

Market capitalisation is calculated by adding up the number of shares a company has and the value of each share.

The classification is also based on how a company ranks in key indices like Sensex and Nifty. For example, the companies in the Nifty Index ranked 101st to 250th are usually considered mid-cap companies. Indian Nifty also has a standard mid-cap index called the Nifty Midcap 50. It holds the 50 most actively traded mid-cap stocks on the market.

Here are some advantages of investing in mid-cap stocks:

In India, mid-cap companies have a better chance of getting loans to raise money than small-cap companies, making it easier for them to grow and expand.

Most mid-cap companies, positioned in the centre of the growth graph, allow for significant dividends and space for value appreciation.

In their early days, most mid-cap stocks weren't looked at very often, so big companies and experienced investors didn't pay much attention to them. It resulted in lower pricing, making them cheaper to incorporate into your portfolio. You can make a lot of money if you can determine which stocks on a mid-cap stock list will likely get more attention and analysis and put most of your money into those funds.

Compared to small-cap companies, these stocks provide enough information about their past and financial health. A list of mid-cap stocks makes it easy to look at companies. You can draw a conclusion about their growth potential and profitability, which will help you decide whether to invest.

Here are some disadvantages of investing in mid-cap stocks:

A value trap occurs when a business keeps making low profits and doesn't have enough cash flow to escape. Value traps can happen to mid-cap companies, especially low-ranking ones, and if the trend lasts for a long time, the companies could go out of business.

Large-cap companies are more likely to have better management and planning systems than mid-cap companies. So, even though they make a lot of money and their value goes up, they might not be able to fully utilise those benefits.

A shaky financial bubble might cause a mid-cap company's tremendous success. Conversely, these companies don't have the money to last when the bubble bursts. So, when looking for the best mid-cap stocks, make sure to look at their financial statement before the bubble to get a good idea of how strong they are financially.

Risk vs. Reward: The risk-reward relationship is what distinguishes blue-chip stocks from Mid-Cap stocks. Blue Chips are a better bet because they are stable and pay steady dividends, even when things are going badly. Conversely, mid-caps, which are risky, offer the chance of higher growth, which makes them appealing to investors who are willing to take more risks.

Market Volatility: Blue Chip stocks tend to be less volatile than Mid-Cap stocks. Their strong financials and established place in the market protect them from market shocks, while Mid-Caps' prices can change a lot.

Investment Horizon: An investor's time frame often affects their choice between blue-chip and mid-cap stocks. Blue Chips are suitable for long-term buyers who want steady returns and growth. Conversely, Mid-Caps may offer big short- to medium-term gains, making them a good choice for investors willing to take more risks and have a shorter investment window.

Diversification: A balanced portfolio that includes both blue-chip and mid-cap stocks is an excellent way to diversify a portfolio. Diversification lowers risk for investors while still allowing them to benefit from the growth potential of Mid-Caps and the security of blue-chip investments.

At the National Institute of Wall Street (NIWS), we have a deep understanding of the intricacies and potential of the Indian stock market, particularly when it comes to making informed decisions about Blue-Chip stocks and Mid-Caps.

Our comparison shows how important it is to ensure that your investment choices align with your financial goals, risk tolerance, and period. Blue Chip stocks are highly valued for their stability and consistent performance, making them an attractive option for investors looking for long-term, low-risk opportunities.

On the other hand, Mid-Cap stocks, known for their potential for substantial growth, appeal to individuals willing to accept higher volatility in exchange for higher returns. When building a well-rounded portfolio, it's essential to consider a mix of Blue Chip and mid-Cap Stocks to strike the right balance between risk and reward.

As experts in the financial industry, NIWS is dedicated to equipping our students and professionals with the necessary knowledge and skills to make well-informed investment choices.

Adopting value investing strategies for long-term growth in India's volatile stock market is both an art and a science. Focusing on undervalued stocks with strong fundamentals is a crucial part of this strategy for unlocking the potential for significant gains.

The National Institute of Wall Street (NIWS) stands out as a top stock market institute in jaipur, Indore, and Delhi as it offers a wide range of courses to help students learn about Finance, Banking, the Stock Market, Wealth Management, Portfolio Management, and both Fundamental and Technical Analysis. NIWS aims to give buyers the information and tools they need to understand the market and make intelligent choices leading to long-term growth.

Here, we will discuss several Value Investing Strategies for Long-Term Growth in India.

Value investing aims to buy stocks when they are cheap compared to their worth and hold on to them until they hit or go above their actual value. It comes from the idea that stocks will increase in value and make money for buyers who buy them when they're cheap and hold on to them for a long time.

Here's a list of several major value investing strategies for tremendous growth in India:

Fundamental analysis is what value investors use to determine a company's worth. Depending on the type of analysis, it may include examining the income statement compared to rivals, the balance sheet, the performance of free cash flow, and valuation metrics. Take our course to discover everything you need to know about fundamental analysis.

Income Statement

Look at a company's past operating profits and the money it made from its primary operations. When you take out things like interest income and interest expense, operating profit shows how well the business plan works.

Profit efficiency can be a solid competitive advantage, so it's best to have high margins compared to your competitors.

Balance Sheet

The balance sheet should show that the business is stable. In order to be a good value prospect, the company must be able to meet its short—and long-term responsibilities. Value investors can determine how good a company is at this by looking at things like the debt-to-equity ratio and the working capital ratio.

Free Cash Flow

If a business pays for its operations and capital spending with cash, it has free cash flow. When a company buys back shares or pays dividends, the money comes from free cash flow.

Value investors want to see a track record of free cash flow growth. When free cash flow goes up and the stock price stays low, it can mean that owners will get good returns in the future.

Valuation Metrics

Comparable ratios, known as valuation metrics, can be used to determine whether a stock is being sold for more or less than it is worth. Two key measures to understand are price-to-book (PB) and price-to-earnings (PE).

PE Ratio

Divide the company's profits per share (EPS) by its stock price to get its PE. You can use the EPS from the previous year or the EPS that you think will be in the next 12 months. The number you get when you use the expected EPS is called the "forward PE."

The PE ratio shows how much it costs the company right now to make one dollar. If the PE ratio is lower than that of a similar competitor, it could be a good deal because you'd be getting the same earnings for less money than the competitor.

PB Ratio

When you compare a company's market value to its book value, which is the value of its assets minus its debts, you get the PB ratio. Divide the stock's price by its book value per share to get the PB ratio.

A PB ratio of less than 1 means the stock might be undervalued. It is especially true in India, where asset-heavy businesses are common.

Quality investing looks for businesses with strong management, low debt, and a history of increasing cash flow. A company's long-term success is often tied to one or more competitive advantages, like size and high margins, unparalleled market penetration, or a brand image that can't be shaky.

Blue-chip stocks and top dividend payers are usually good choices if you're looking for quality stocks.

Quality stocks don't have as much room to grow as smaller, new companies. For this reason, investors may not pay as much attention to them as other, more exciting investments. It could cause the price to drop too low. On the other hand, quality stocks do better in bad times than stocks of companies that aren't as well established.

When you do contrarian trading, you buy stocks that aren't popular at the moment, which goes against the current market trend. The important thing is to find companies that are fundamentally strong but have been unfairly penalized by the market. This method can work exceptionally well in India's volatile markets, where changes in the economy, new rules, or short-term setbacks can significantly affect stock prices.

In India, investing in companies that regularly pay high dividends can be a good idea because those companies are usually seen as more financially stable and less risky. When you invest in dividends, you get regular income and the chance that your money will grow. However, it's important to ensure that dividends are sustainable and backed by strong free cash flows.

Here are some essential things you should know about value investment for long-term gains:

The price differential between a stock and its intrinsic value is known as the margin of safety. The higher the margin of safety, the better protected you are from making a mistake in your value judgment.

You are safe as long as you buy the stock for INR 90 when you think it should be worth INR 100. In the Indian market, this means doing extensive research to find undervalued companies with strong fundamentals, such as solid earnings, low debt, and long-term business models.

For your value stocks, choose a minimal margin of safety. Twenty percent is a good starting point, and it can be changed up or down based on your needs.

Another way to protect yourself from being wrong about a stock or its future is to spread your investments. Maintaining a diverse range of stocks is an excellent way of risk management as it protects your savings from any one asset.

Always keep 20 different stocks in your portfolio at the same time. Select equities with varying risk profiles as much as you can. You can put your money into different currencies, businesses, and market caps.

Value investing is typically a long-term plan. The Indian stock market can be very volatile, which tests an investor's patience. It's essential to stay focused on the long-term prospects of your investments and not give in to the urge to respond to short-term changes in the market. Companies with strong fundamentals may take time to reflect their true value in the stock market.

Markets go to extremes when people's feelings take over. Fear causes markets to crash, and greed causes stock market bubbles.

It's possible to make money during market extremes if you can stay calm and not follow the crowd, which is easier said than done. If you follow the crowd, on the other hand, you're more likely to buy high and sell low. Putting money into that way is not a good long-term strategy.

Value investing in India is a great way to achieve long-term growth because it uses disciplined, research-based methods to tap into the market's natural potential. Investors can lower their risk by focusing on undervalued stocks with strong foundations and taking advantage of the Indian economy's growth.

At NIWS, we're dedicated to helping our clients navigate this path by blending deep market knowledge with a clear focus on creating value. Let's start this journey together towards long-term growth and wealth building. Contact NIWS immediately to find out how we can help you reach your business goals.

Demat account opening is crucial since digital trading is done. Demat account-based share sale and purchase has made the process easier for investors as they do not have to stand in queues or fill out lengthy forms to open an account. Stock investment, which requires a Demat account, can be online. It is the easiest way to open an account online, so you can open a Demat account in a few simple steps. This account type digitally stores your share when you consider online trading.

Since opening a demat account requires a few simple steps to initiate trading in the stock market, NIWS, the leading stock market trading courses in delhi, Jaipur, and other places, helps you understand how to open a demat account to initiate stock investments.

When trading and investing in stocks in India, a Demat (Dematerialised) account is required. This account replaces traditional physical share certificates with electronic certificates, making transactions convenient, secure, and faster. The reasons given below explain why a Demat account is needed.

It eliminates the risk of theft, damage, or loss in the case of physical share certificates.

As far as buying and selling are concerned, the Demat account helps engage in this and holds the securities electronically.

A demat account will always be cost-effective as it helps eliminate paperwork that may incur additional costs. A person can access a wide range of financial instruments, such as mutual funds, government securities, bonds, and equities, through a Demat account.

There are a few steps that you must follow to open a Demat account, and they’ve been mentioned as follows:

You will first have to select a registered Depository Participant, which may be any brokerage firm or a bank with the authority to open Demat accounts.

Once you choose a Depository Participant, you will have to fill out a form that your DP provides. The form will have fields for you to mention your personal information, such as contact information, KYC details, and others.

KYC, the 'Know Your Customer' verification process, has to be done by submitting the necessary documents, such as an Aadhaar Card, Passport, Voter ID, or PAN card, and then KYC verification is successful.

The Depository Participant is responsible for verifying the submitted documents and checking the details you have filled in the application form.

You may encounter some outlined terms and conditions, which you will have to sign. Once you do that, your Demat account opening will reach the last process of account activation.

Once all the information is verified and no document is left to be submitted as per the requirement, your DP will provide you with the account details that you can use along with the login credentials for your Demat account for you to access from now on.

Different charges apply to having a Demat account and maintaining it throughout the year. Let’s know about them:

It is a one-time fee that your Depository Participant may charge for setting up the Demat account, and the amount may vary for each Depository Participant.

Of course, your DP will levy an annual fee to maintain your Demat account. This fee will cover the cost of record-keeping, account maintenance, and other relevant expenses that DP has to incur.

DP also imposes different transaction fees for buying and selling securities, and the Stock Exchange may charge you through a Demat account.

For transparency, always clarify your doubts regarding transaction charges before opening a Demat account. These charges are also variable, depending on the volume and type of transactions.

The charges apply when you debit securities from your Demat account, especially when you sell your shares. DP also facilitates the transfer of securities out of your Demat account, and as a result, it may charge a certain amount.

Various types of documents are required to open a Demat account, and they have been mentioned in the details below. The four different types of documents that you need to submit when you want to open a Demat account are as follows:

Any one of the following documents is required to submit for proof of identity to open a Demat account.

Aadhaar card

Pan card

Passport

Driver’s license

online government-issued photo identity card

Voter id

Any one of the following documents is required for proof of address:

Aadhaar card

Passport

Driver’s license

Voter ID card

Utility bills which include gas, water, or electricity bills (should not be older than 3 months)

Rent Agreement

Ration card

They must also submit a passport-size photo

Salary slip

bank statements

Income tax returns

All these requirements may vary depending upon the Depository Participant, and all the documents must be up-to-date and valid.

A few crucial points need to be kept in mind if you want to invest in stocks and get good returns. Let’s know some of the essential points given as follows:

You must understand the stock market's variable factors and the risks involved. You need to make yourself fundamentally strong regarding stocks, have some investment strategies, and be an expert in technicality and stock market trends.

Having a reputable brokerage firm will help you get good returns on your investment. A good broker may offer trading services linked to Demat accounts, which will definitely be beneficial in the long term.

You must start transferring funds to your trading account linked with the Demat account. Once you can use the platform and understand the options given in your Demat account, you can place buy or sell orders according to your preference for investment.

If you want to know how your investment is doing in your Demat account, you must monitor it per the market trends to understand your performance. You must stay up-to-date with the financial news and announcements, which will be great if you want to make good returns on your investment.

The term "demat account" or "dematerialization account" refers to an easier method of storing bonds, shares, mutual funds, government securities, mutual funds, exchange-traded funds (ETFs), and insurance. Demat Accounts lower the possibility of damage or loss by eliminating the requirement for physical share certificates.

NIWS, the well-known stock market institute, provides this guide to help investors start investing in stocks. It explains the need for a Demat account and the process of opening one.

The abundant alternatives can appear confusing to those new to the complex stock market and investing world. Exchange-traded funds, or ETFs, and mutual funds provide many investment possibilities.

Mutual funds are a popular option if you want to invest in broad portfolio assets, such as bonds, stocks, or others, and pool your money with others. This resource sharing makes many securities available to investors, including small ones.

Unlike mutual funds, exchange-traded funds or ETFs have specific unique characteristics. Similar to individual stocks, ETFs are traded on stock markets. So, you can sell and buy ETF shares at market prices the entire trading day.

Since mutual funds and exchange-traded funds (ETFs) equally have crucial roles in the investing landscape to meet the investors' different needs, NIWS, the stock market course in indore, Jaipur, and many other places across the Indian region explains both in stock market investing to help you choose the ideal one.

Funds invested in money market instruments, stocks, bonds, and other assets are purchased by a group of investors by pooling their funds. Investment managers often manage the assets to provide investors with the returns they generate, and investors purchase shares in mutual funds.

Diversification in mutual funds refers to investment options in geographic regions, asset classes, and industries. When investors diversify their investments, they minimize their exposure to a single market or asset. When their assets are spread out, their risk is also diversified.

A portfolio that includes a variety of investment instruments, such as bonds and stocks to cash mutual funds, must be created by the investor. Then, the risk elements of different investment schemes must be sorted by choosing securities with diversified risk levels. So, when you experience loss in a single element, you can get profit from other elements.

Investors who lack experience or time to manage their assets may find mutual funds useful for professional research and management. Mutual funds are managed by experienced professionals who have the resources and expertise to monitor, buy, and sell investments. These managers make decisions on behalf of fund investors through extensive market research and analysis.

Your fiscal progress graph depends on professional management since fund managers effectively manage portfolios of mutual funds. The risks involved while ensuring compliance, selecting securities, implementing relevant fund strategy, protecting investments, and much more.

Cost benefits or economies of scale occur when businesses increase their output and become more productive or efficient, which enables cost savings. The earnings generated by mutual fund businesses are dependent upon economies of scale. These benefits resulting from higher operational scale or increased production could benefit mutual funds.

Investing opportunities and risk exposure can be optimized by liquidity investors, making it simple to reallocate money among various asset classes. A mutual fund's liquidity is based on the liquidity of its assets.

How simple it is to sell or buy mutual fund units without depressing the fund's market value is called liquidity.

The range of offerings simply refers to the available range of funds for selection. Funds that invest in bonds, stocks, or those who combine them are included in these funds. Investing is made more accessible for investors who can choose from an extensive choice of funds to meet their financial objectives.

Investors can make the best choice depending on their financial goals and the risk they can take while creating a solid investment strategy when they have a range of options.

An exchange-traded fund (ETF) is designed to replicate a specific market index, which gives rise to the passive management style of fund management.

ETF trading is possible if the exchange is open, while their price also adjusts all day. It allows investors to place orders in many ways and make investment decisions promptly. People investing in ETFs have every investing trading combination in common stocks, such as stop-limit orders and limit orders

The lack of recurrent charges can reduce ETF returns, and a lower expense ratio makes ETFs a cost-effective investment option. ETF management entails less administrative expense than mutual fund management. ETFs are sold and purchased on the open market. Thus, a shareholder's selling of shares does not impact the fund. Market-based trading allows ETFs to minimize their operating and administrative costs.

The way that shares are issued and redeemed in response to market demand accounts for the tax efficiency of ETFs. These investment vehicles have better tax profiles due to the in-kind redemption process and tax efficiency.

ETFs provide transparency and easier access to their holdings. Transparency facilitates ensuring investors receive a fair price, helping maintain an ETF share's price in accordance with the underlying portfolio's net asset value (NAV).

Selling or buying a collection of assets during market hours through ETFs helps diversify your portfolio and reduce risk. With ETFs, you can own investments in niche sectors, commodities, and foreign markets, diversifying your portfolio beyond typical bonds and stocks.

Mutual funds and ETFs might be affected by the market and the risks associated with underlying assets, such as investing in foreign equities, fixed-income instruments, smaller businesses, and commodities.

Mutual funds handle all orders at the closing NAV, which provides end-of-day liquidity. At the same time, investors can transact due to the intraday liquidity provided by ETFs' real-time trading feature all day. ETFs and mutual funds facilitate stock transactions by pooling the money of many participants.

Based on variables such as demand and supply, price discovery assists investors in determining the appropriate market price for securities or other assets. ETFs and mutual funds contribute to determining fair values for stocks by continuously selling and buying stocks to comply with investor demand.

A variety of stocks, ETFs, and mutual funds enable every investor to participate in the stock market. Therefore, many investors can access the stock market regardless of their experience level.

Mutual funds and exchange-traded funds (ETFs) equally have crucial roles in the investing landscape to meet the needs of investors. Risk tolerance, time horizon, financial goals, and trading preferences significantly influence the choice between ETFs and mutual funds.

Mutual funds offer active management and enhanced diversification, while ETFs offer reduced expense ratios, tax efficiency, and liquidity. Both investment vehicles have many benefits, and investing in any of them depends on the investors' objectives and investment plans. Although both are beneficial, you must consider specific investment risks while investing.

NIWS guides and helps investors make informed decisions about creating a well-structured and diversified portfolio by explaining the roles of these two investment vehicles and effectively managing potential investment risks. Reach out to NIWS, the National Institute of Wall Street, today, and make wise investment decisions by getting professional guidance and support from its experts.

Are you interested in learning about tax planning? If so, this blog is the right place to start. Proper financial analysis is essential to ensuring tax efficiency. The process of examining a financial situation and making a strategic decision to minimize tax liabilities is known as tax planning.

Tax planning is essential for all businesses, but it is mandatory when investing in the stock market due to the potential for huge gains and tax implications. By strategically managing the tax liabilities, you can-

To know more about tax planning and stock market gains, let’s explore the sections in this blog below.

Stock market gains refer to increased stock market value from their purchase price. There are two different kinds of market gains-

Dividend income refers to the proportion of the company's revenue distributed to all the shareholders as a reward for owning the shares.

When companies declare dividends, the earnings distributed to shareholders are per-share.

Let's discuss the factors which influence the Stock Market Gains in India-

Market condition is a considerable element that influences stock market gains. This condition can include the following -

Factors such as investor behavior, market sentiment, and investor confidence play a huge part as well. High volatility in the market can increase the chances of trading opportunities, but it also comes with higher risks.

Economic factors such as GDP, inflation rate, interest rate, etc., can easily influence the stock market. When the GDP is strong with very low unemployment, it positively affects company profits and stock prices.

We all know tax planning is a critical task in stock market investments. There is almost no room for error, as the planning directly affects the overall returns and portfolio performance. Let's discuss some of the reasons which justify the importance of tax planning-

Some of the strategies that can be used for Tax Planning in the Stock Market-

Some of the challenges in Tax planning involve-

NIWS is a stock market classes indore and Delhi that offers career-oriented online and offline courses for investors and traders. It offers course modules in Banking, finance, stock market, portfolio, and Wealth management.

Connect with NIWS to learn more about how trades work and what strategies can be implemented while planning long-term investments. It is the finest stock market institute in India, and it has helped many individuals kick-start their careers in the stock market by teaching them about it.

Tax planning is a critical component of wealth management. It can help investors minimize risk, as every strategy is developed after thorough market research and maximizes returns. You can start with tax planning using the methods mentioned above. But keep in mind that it also has risks associated with it. Sometimes, market volatility leads to losses you may not be ready to bear.

To learn more about tax planning, connect with NIWS.

Ready to level up your investment game? Not every app you see in advertisements might be right for you. With new apps approaching the market every day, each with dissimilar features, it can be challenging to deduce which one is the right fit for you. The Indian stock market essentially differs from foreign markets in structure and regulations. In such cases, trading apps suitable for other markets might be irrelevant here.

This article analyses 10 of the best trading apps for Indian Investors. We assessed the apps pertinent to the diverse Indian market. Trading platforms are integral to keeping track of the market and managing profiles, whether for beginners or experts. Here are ten leading trading platforms and apps suggested by NIWS for beginners to start with.

If you want to deepen your understanding and skills, consider enrolling in a stock market course in Jaipur with NIWS. Their comprehensive courses are designed to equip you with the knowledge and tools needed to navigate the complexities of the Indian stock market effectively.

Here, we suggest some of the best stock market applications and trading platforms for Indian investors. It would help if you first choose the appropriate investing application and trading platform to succeed in the specific sector.

Entrepreneur and filmmaker, Shripal Morakhia of India, founded Sharekhan in February 2000. The company was rebranded as Sharekhan following its acquisition in 2017 by the French international banking institution BNP Paribas. Sharekhan is a trading and investing platform. The platform reportedly had about 6,94,334 active clients in the fiscal year 2022–2023. Sharekhan provides the opportunity to open a free Demat account to begin trading.

The Process Of Creating A Trading Account

To open a Sharekhan’s free Demat account, you'll need a PAN card copy, aadhaar Card copy, proof of address- ration card/passport/driving license/bank statement of 2 months, cancelled cheque leaf with the name printed on it or the passbook's first page & latest transaction, two passport-size photographs.

You can open a Demat account through their official website or visit their nearest branch using these documents.

Paytm Money is Paytm’s company. It made its debut in 2018 as a part of Paytm. It is a global Noida-based fintech company. Vijay Shekhar Sharma, the CEO of One97 Communications, the business that powers Paytm, created it in 2010. One97 Communications is Paytm's parent company.

In addition, it offers investment options through initial public offerings or IPOs and depository services. Paytm Money is registered with the Indian Securities and Exchange Board as a stock brokerage platform and repository participant.

The Process Of Creating A Trading Account

Raamdeo Agrawal and Motilal Oswal established the firm in 1987 as a brokerage business. When electronic transactions became common, the corporation used online trade offers. It provides many goods and services, including commodities, stock, initial public offerings (IPOs), mutual funds, investment advising, and portfolio management to help investors with their stocks.

The Process Of Creating A Trading Account

Harsh Jain, Neeraj Singh, Lalit Keshre, and Ishan Bansal started Groww in 2017 in Bangalore, India. It originally served as a direct distribution channel for mutual funds. Groww began offering stock access, ETFs, digital gold, IPOs, and intraday trading in 2020.

The Process Of Creating A Trading Account

Nirmal Jain started IIFL with support from investor Prem Watsa from Canada, General Atlantic, a private equity firm, and CDC Group, the UK government's private equity division funds IIFL. One of India's seven biggest banking companies, IIFL, or India Infoline Finance Limited, is the most profitable independent financial services provider.

The Process Of Creating A Trading Account

Use the 'Open Account' tab on the IIFL Securities’ to initiate the opening of a demat account.

The platform provides a complimentary demat account opening service and waives maintenance fees for the account's first year.

After completing the online form and verifying it, you must submit scanned copies of your PAN and Aadhar card to create a Demat account.

Brothers Nikhil and Nithin Kamath started the business in August 2010. Zerodha, an Indian-based stockbroking and financial services company, offers brokerage services to individual and institutional clients and trading in mutual funds, bonds, currency, and commodities.

The Process Of Creating A Trading Account

Angel One Limited, established in 1996, is an Indian brokerage business formerly known as Angel Broking Limited. Its offerings range from investment advising to depository services, online stock broking, commodities trading, distribution of mutual funds, initial public offerings, and portfolio management. The company provides several online trading applications.

The Process Of Creating A Trading Account

HDFC Securities Limited is a subsidiary of HDFC Bank. It launched in 2000 and is based in Mumbai. HDFC Securities is India's most significant private-sector lender's stockbroking arm. It started as an HDFC Bank, HDFC, and Indocean eSecurities Holdings joint venture. They provide investing options in stocks, mutual funds, SIPs, IPOs, derivatives, bonds, NCDs, corporate FDs, ETFs, bullion, metals, energy, and agricultural commodities.

The Process Of Creating A Trading Account

HDFC Securities offers an all-in-one trading account with zero charges to open from the HDFC securities website.

5paisa was first launched in 2016 by its CEO, Narayan Gangadhar. It offers investment opportunities in the share market, mutual funds, IPOs, EFTs, SIPs, indices and bonds. 5paisa provides three types of demat trading accounts. The regular account costs nothing, but the power investor and ultra trader accounts cost 599 and 1199 INR, respectively.

The Process Of Creating A Trading Account

Kotak Securities Limited uses a single login platform to provide comprehensive investment services for various asset types, such as debt, stock, mutual funds, commodities, and currencies. It was founded in 1994 as a part of Kotak Mahindra Bank.

The Process Of Creating A Trading Account

All of the platforms mentioned above are well-established in India, ensuring safety. But, certain risks are involved in the actual trade. Each trade involves a separate set of risks. Therefore, we advise reading the fine print before investing.

In this article, we have suggested the top stock market apps in operation and provide you with all possible resources to make informed decisions. Though market knowledge is essential to survive in stock markets, NIWS suggests that pre-investment research is necessary. Well-researched investments will help you grow your investment portfolio and maintain wealth.

Start with a demonstration class.