Market indices bring together a select group of company stocks and regularly measure them to show the performance of the overall market or a certain segment of the market.

There are thousands of companies listed on stock markets, making it almost impossible to monitor each company. This is why stock market indices are created.

In short, an index helps investors understand the health of the stock market, enables them to study the market sentiment and makes it easy to compare the performance of an individual stock.

Sensex and Nifty are the two most important stock market Indices in India. They are the benchmark indices meaning, the important ones, and a standard point of reference for the entire stock market of India.

For example, the BSE Sensex is an index consisting of 30 stocks. Similarly, the BSE 500 is an index consisting of 500 stocks.

KEY TAKEAWAYS

S&P BSE Sensex, a collection of 30 best-performing stocks, and Nifty 50, a collection of 50 best-performing stocks are indicators of BSE and NSE respectively. They are considered benchmark indices because they are the most concise, use the best practices to regulate the companies they pick, and hence are the best points of reference for how the markets are doing in general.

NSE Indices Limited (formerly known as India Index Services & Products Limited), or NSE Indices, owns and manages a portfolio of 67 indices under the NIFTY brand as of September 30, 2016, including NIFTY 50. NIFTY indices are used as benchmarks for products traded on NSE.

NIFTY indices served as the benchmark index for 38 ETFs listed in India and 12 ETFs listed abroad as of September 30, 2016. Derivatives benchmarked to NIFTY indices were also available for trading on four international stock exchanges as of November 30, 2016 (The Singapore Exchange, the Chicago Mercantile Exchange, the Taiwan Futures Exchange and the Osaka Securities Exchange).

Sensex, otherwise known as the S&P BSE Sensex index, is the benchmark index of India's BSE, formerly known as the Bombay Stock Exchange.) The Sensex is comprised of 30 of the largest and most actively traded stocks on the BSE, providing a gauge of India's economy.

Created in 1986, the Sensex is the oldest stock index in India. The index's composition is reviewed in June and December each year. Analysts and investors use it to observe the cycles of India's economy and the development and decline of particular industries.

|

Fun Fact: BSE adds S&P as a prefix before all the indices because, in the year 2013, BSE and S&P Down Jones Indices, a global resource for all index related information announced a strategic partnership “to calculate, disseminate, and license the widely followed suite of BSE indices,” BSE had said in a statement. It is just a co-branding technique. To learn how to use an index for benchmarking portfolio performance join NIWS Best share market course in Jaipur

|

Market-Cap Based Indicies

Market cap is the market value of any public traded company. There are few indices that purely select companies only on the basis of market capitalization.

Indices like NSE small cap 50 and S&P BSE small-cap are indices that are a collection of only those companies that have a lower/smaller market capitalization in accordance with rules by SEBI. There are also other indices like NSE midcap 100, S&P BSE midcap, and likewise.

Sectoral Indicies

NSE and BSE also have some indicators that are a gauge of companies falling under one particular sector. Indices like NSE Pharma and S&P BSE Healthcare are indicators of their respective exchanges for the pharmaceutical sector.

It is not necessary that both the exchanges will have corresponding indices for all the sectors but this is generally the case.

Another example could be Nifty PSU Bank and S&P BSE PSU Indices are indicators of all the listed public sector banks.

Other Indicies

There are also some other indices like S&P BSE 100, S&P BSE 500, and NSE 100 among others which are slightly bigger indices and have a much bigger number of stocks listed on them.

Till now we understood, what are stock market indices and their examples but do we know how a stock market index in India selects stocks.

When an entire index, for e.g. a Sensex or a Nifty goes up or down, it means that stocks comprising those indices have performed better or worse. This does not mean that if a company, say Reliance Industries Ltd. (RIL) which is listed in both, the Nifty and Sensex, goes up by say 5% during a trading session, the index will not correspondingly go up by 5% because there are other stocks in the index as well which may have gone up or down and influenced the movement of the index.

How will the weights be assigned depends on the stock selection strategy put in place? On any given day, not all sectors in the economy are doing well. An index’s total value cannot be a simple addition of all m-cap values because not all stocks carry the same weightage in the index

There are primarily two factors by which stocks are picked:

Companies with the largest market cap are picked and grouped together in an index when the M-cap is the premise of the stock selection strategy.

Companies with the largest m-cap have a bigger weightage on the index’s value while stocks with a small m-cap do not influence the index as much. Indian indices mostly use free-float market capitalization for assigning weights to their stocks.

There are also some indices in the world that use price to give weightage to stocks in an index.

An example of this would be Japan’s Nikkei 225. Companies with a higher stock price have a higher weightage and impact the index more than the lower valued stocks.

Note:

M-cap is the total value of the company measured in the outstanding shares it has issued. Free float m-cap, which the indices use to weigh stocks, excludes shares held by promoters.

For example, Reliance Industries Ltd. (RIL) has the highest free float m-cap as on April 20 closing data so it has the highest weightage among other stocks that form Sensex. So a movement in RIL, positive or negative, will have a higher impact than a positive or negative movement in other stocks.

The basic premise of having indices is to make trading easy for investors.

Imagine a stock market where you do not have such categories, where all the stocks listed on the exchanges are available for purchase, you do not know which stock has a higher m-cap, or lower value and which are the ‘better’ stocks. This is where the importance of stock market indices is realized.

They make it easy for you to trade by grouping them and making their visibility stronger.

Here are a few reasons why having indices is an essential component of stock market investments:

Let’s consider Sensex as an example. S&P BSE Sensex is a collection of 30 stocks, S&P BSE 100 is a collection of 100 stocks, and S&P BSE 500 is a collection of 500 stocks. These indices help you to see the top stocks by way of m-cap in one place.

For example, in current times when a pandemic has gripped the entire world and stock markets are down, you may be curious about how the health sector is doing. In the absence of indices, you would have to hunt for all pharmaceutical companies individually, collate them together, and do your own math.

However, grouped indices like Nifty Pharma and S&P BSE Healthcare do that job for you.

Indices have a plethora of information on stocks. Price history, volume changes, peer-to-peer comparison, sector performance, volatility, and a sense of where the market is moving. If a collection of the 30 or 50 best companies shows an uptrend or a downtrend, it speaks volumes about how the stock market is generally doing.

If we refer to the table above, we can see that in the calendar year 2020, the Nifty 50 has dropped 26.59% and Sensex by 26.07% in the last 4.5 months. This speaks a lot about investor sentiment.

The coronavirus has shaken investor confidence and global economies. With job loss, industry shutdowns and the lockdown imposed, people have lower confidence in the markets and do not consider them as safe havens anymore. Currently, the market is indicating a negative investor sentiment.

|

Index |

YTD performance (year to date) * |

|

Nifty 50 |

-26.59% |

|

S&P BSE Sensex |

-26.07% |

*As of April 20 closing session

An index’s value depends on whether it is a price-weighted index or a market-cap-weighted.

Below is an example of the BSE Sensex to understand how an index is calculated.

Stock market indices are the bread and butter of the investment milieu. It is not just an added advantage but a necessity.

Having indices reduces your load and makes at least the first step in stock market investment easy. This is not the end. You do need to do the rest of the work for yourself regarding investing.

Investment portfolios cannot be one-size-fits-all and need to be tailor-made for every investor.

Jobbing in the stock market is a term that means making quick profits on small moves of a stock. The more common terms for the same used in the stock markets nowadays might be scalping, day-trading, high-frequency trading, etc.

Jobbing in share market refers to achieving results by increasing the number of winners and sacrificing the size of the wins. A scalper, or someone engaged in jobbing in the stock market, intends to take as many small profits as possible. This is the opposite of the "let your profits run" mindset, which attempts to optimize positive trading results by increasing the size of winning trades.

So, what is jobbing in stock market? It's a strategy focused on making frequent, smaller profits rather than holding for larger gains.

Stock jobbing is a British slang term for short-term day trading where the trader tries to make frequent small profits. These individuals were actually market makers on the London Stock Exchange before October 1986 when London's financial sector was deregulated.

While most investors assume it is better to seek value through long-term investments, stock-jobbing (day trading) takes on a more speculative short-term goal. As opposed to using fundamental analysis and selecting investments that professionals believe are likely to grow in price over time, the short-term trader seeks to identify and take opportunities to make quick, small profits and replicate that procedure with as great a frequency as possible.

Stock jobbing types will often use technical analysis to generate short-term gains. High-frequency traders are the most modern version of stock jobbers because they seek to identify, fill and match orders in tiny fractions of a second.

Jobber, also called “stock jobber”, act as market makers. They hold shares on their own books and create market liquidity by buying and selling securities, and matching investors’ buy and sell orders through their brokers, who were not allowed to make markets.

A jobber is a professional speculator, and buys and sells shares for himself. He does not have any clients. His business is to speculate on which way prices are moving and make a quick profit on it. He does not want to buy shares and keep them for the long term as investors do. But, to do business on the floor of the stock exchange, he needs to have a broker as a sponsor. He shares a part of his profit with the broker under a pre-decided agreement.

The jobbers are also known as tarawaniwallas. The Jobber market is essentially a wholesaler who operates on a small scale or who sells only to retailers and institutions.

To be a successful jobber, one had to be very good at mental arithmetic. If you were jobbing in more than one or two stocks, then your skills needed to be even sharper. That is because you were carrying an inventory of shares at all times, irrespective of whether you were long (had a buy position) or short (had a sell position) on a stock.

Tasks of a Jobber in Share Market

Role of a Jobber while Placing an Order

There are 3 Parties involved in the dealing of shares:

The stock broker simply acts as agent and contacts the particular jobber in the stock exchange on behalf of the client. He does not disclose to the jobber whether he is a buyer or seller of shares. He therefore, asks him to quote two prices:

Example: Mr. Arnav wants to sell 1000 shares of a company. He contacts a broker dealing on the stock exchange. The broker asks a jobber to give quotations. He does not disclose the jobber whether he wants buy or sell the shares of the company. The jobber gives two prices, one at which he is ready to sell and another at which he is ready to buy.

If the broker is not satisfied, he can go to another jobber or ask the first one to make it closer (i.e. to reduce the margin between buying and selling). If the broker is satisfied with the new quotation, he then contacts with his client, informs him the bid of the share. If the client agrees to bid the price, then bargain is struck.

A jobber helped create liquidity in a stock by offering two-way quotes and also helped in price discovery. He took on the risk, confident that he would be able to sell whatever he bought and buy back whatever he sold.

A jobber would buy from you at a rate lower than what he would sell to you for, and the difference or “spread” as it was known, would be his profit. The spread quoted by the jobber would depend on the quantity of shares you wanted to buy from him or sell to him – the smaller the quantity, the less the spread, and the bigger the quantity, the wider the spread. A jobber had to ask for a higher spread while dealing in big quantities since the risk he took was higher.

It was not just enough to remember the number of shares you were long or short on; you had to remember the average buying or selling cost of those shares. That in turn would decide the bid-ask spread (“bid” is the price quoted by the buyer and “ask” by the seller) a jobber quoted.

I knew of expert jobbers who could memorise their inventory and the average price of trades in nearly two dozen stocks without having to check their deal pads.

A good jobber also had to be a skilled psychologist because he is trained from well renowend share market classes in Indore. It required him to be able to size up a prospective counterparty and gauge whether he was a likely buyer or seller. His profit margin would hinge on his ability at this.

A typical conversation between the two would run on these lines:

“What is the quote for Arvind Mills? “57-60.” (I will buy from you at 57 and sell to you at 60) “What quantity is this valid for? “500 shares.” “I want to sell 500 shares.” “Okay, bought 500 shares from you at 57.

Does your quote hold good for another 500? “Yes.“ Okay, I want to sell another 500 shares.” “Bought 500 from you at 57.

I want to sell another 500.What’s your quote? ”56-59.” Okay, I am selling 500 more to you.” “Bought 500 from you at 56.“

How about 500 more? “55-58.”

This Quotes are also called ‘Double barrelled price ‘ or ‘Jobbers Turn’

As the client keeps selling more, the jobber in the stock market will keep lowering the bid-ask quotes, but not necessarily the spread, which will remain Rs 3. That is because the jobber is now running up a plus-position, and his profit will depend on how cheap he can get the shares.

The more heavily traded the stock, the smaller will be the jobber’s spread, because there will be plenty of buyers and sellers. For an illiquid stock, the spread would be wider, and at times even outrageous if a jobber enjoyed a near monopoly in that stock. There were different categories of jobbing in share market participants, depending on the risk they were willing to take.

Jobbing in the stock market was always in demand because brokers preferred to deal with him rather than with each other. Since jobbers played for small profit margins by trading as many times as possible, brokers had the comfort that they would not be overcharged.

If a broker was buying on behalf of a promoter using some inside information or buying a huge block of shares for an institution, he would, after the trade, casually tell the jobber something like, “Don’t keep your position open for too long,” or “Take your profit and move on quickly.” An honest jobber would then try to close out his position quickly and not take up a position on the same side as the broker so as to profit from the information.

Brokers looking to buy or sell large blocks were often at the mercy of jobbers, and it was to the credit of the jobbing community that a great majority of them did not misuse this power.

| Jobber | Broker | |

| Meaning | A jobber is an independent dealer, purchasing or selling securities, on his own account | A broker is an agent who deals with the jobber on behalf of his client. In other words, a broker is a middleman between a jobber and clients. |

| Nature of Trading | A jobber carries out trading activities only with the brokers | A broker carries out trading activities with a jobber on behalf of his investors. |

| Restriction on Dealings | They are prohibited to directly buy or sell securities in the stock exchange, also he cannot directly deal with the investors as he is not a member of the exchange. | They act as a link between jobbers and investors, i.e. buying and selling securities on behalf of their investors. |

| Agents | A jobber is a special mercantile agent providing two - way quotes | A broker is a general mercantile agent and trade on behalf of their clients. |

| Form of Consideration | They get consideration in the form of profit from market-making and profit-sharing | They get consideration of commission or brokerage |

Financial derivatives have changed the finance world by creating innovative ways to comprehend, measure, and manage risks. Derivatives are meant to facilitate the hedging of price risks of inventory holdings or a financial/commercial transaction over a certain period. By locking in asset prices, derivative products minimize the impact of fluctuations in asset prices on the profitability and cash flow situation of risk-averse investors and, thereby, serve as risk management instruments. The derivative market was introduced in India in 2000, and since then, it has gained great significance like its counterpart abroad.

“ Derivatives are financial securities and contracts that obtain value from something else, known as underlying securities. Underlying securities may be stocks, currency, commodities, bonds, etc.”

By providing investors and issuers with a wider array of tools for managing risks and raising capital, derivatives improve the allocation of credit and the sharing of risk in the global economy, lowering the cost of capital formation and stimulating economic growth. Now that world markets for trade and finance have become more integrated, derivatives have strengthened these important linkages between global markets,

increasing market liquidity and efficiency and facilitating trade and finance flow.

Derivatives can be used for several purposes, including insuring against price movements (hedging), increasing exposure to price movements for speculation/trading, or accessing otherwise hard-to-trade assets or markets. Some more common derivatives include forwards, futures, options, swaps, and variations such as synthetic collateralized debt obligations and credit default swaps.

Derivatives can either be exchange-traded or traded over the counter (OTC)

Exchange refers to the formally established stock exchange wherein securities are traded and they have a defined set of rules for the participants. Whereas OTC is a dealer oriented market of securities, which is an unorganized market where trading happens by way of phone, emails, etc.

Why should you invest in the Derivatives Market?

A derivative product can be structured to enable a pay-off and make good some or all losses if gold prices go up as feared.

Trading in the Derivatives Market

If you are new to Derivatives and have prior knowledge of the stock market, follow these simple steps before you start trading in derivatives. Hence, you can also join the share market training in Indore for proper guidance in the stock market under the well-experienced faculty, including the derivatives market.

Note: Trading in the derivatives market is very similar to trading in the cash segment of the stock markets. This has 3 key prerequisites –

What are the Types Of Derivatives?

The main instruments for derivatives trading in India are futures contracts, options contracts, swaps, etc. These instruments are originally meant for hedging purposes. However, their use for speculation can't be ruled out.

A forward contract or simply a forward is a non-standardized contract between two parties to buy or to sell an asset at a specified future time at an amount agreed upon today. The party agreeing to buy the underlying asset in the future assumes a long position, and the party agreeing to sell the asset in the future assumes a short position.

Example :

Suppose you must buy some gold ornaments, say from a local jewellery manufacturer, XYZ Gold Inc. Further, assume you need these gold ornaments some three months later, in December. You agree to buy the gold ornaments at INR 54000 per 10 grams on 15 March 2020. The current price, however, is INR 53600 per gram.

This will be the forward rate or the delivery price from XYZ Gold Inc. four months from now on the delivery date.

This illustrates a forward contract. Please note that there is no money transaction between you and XYZ Gold Inc. during the agreement. Thus, no monetary transaction takes place during the creation of the forward contract. The profit or loss to XYZ Gold Inc. depends rather on the spot price on the delivery date.

Now assume that the spot price on delivery day becomes INR 54100 per 10 grams. In this situation, XYZ Gold Inc. will lose INR 100 per 10 grams, and you will benefit the same on your forward contract. Thus, the difference between the spot and forward prices on the delivery day is the profit/loss to the buyer/seller.

|

Future Contract |

Forward Contract |

|

Traded on Organized Stock Exchange |

Over the Counter (OTC) in nature |

|

Standardized contract terms, hence more liquid |

Customized contract terms, hence less liquid |

|

Required margin payments |

No margin payments |

|

Follow Daily Settlement |

Settlement happens at the end of the period |

Along with some exceptions to forward contracts, there are future contracts. What makes future different forward contracts is that we trade futures on stock exchanges while forward on the OTC market. OTC, or the over-the-counter market, is a marketplace for typically forward contracts.

An option is a contract which gives the buyer (the owner) the right, but not the obligation, to buy or sell an underlying asset or instrument at a specified strike price on or before a specified date. The seller has the corresponding obligation to fulfil the transaction, that is, to sell or buy if the buyer (owner) & exercises the option. The buyer pays a premium to the seller for this right. An option that conveys to the owner the right to buy something at a certain price is a "call option"; an option that conveys the right of the owner to sell something at a certain price is a "put option."

Example:

Consider the same example. Let us now suppose that the seller, XYZ Gold Inc., believes that the spot price may rise above INR 54000 per 10 grams during your forward contract agreement. So, to limit loss, XYZ Gold Inc. purchases a call option for Rs. 1050 at the exercise price of INR 54000 per 10 grams with a three-month expiration date.

The exercise price is technically known as a strike price. Similarly, the price of the call option is technically known as the option price or the premium.

The call option gives the buyer the right to buy the gold at the strike price on the expiration date. However, there is no obligation to buy on the expiration date. He may or may not exercise his right on the expiration date. If the price is in the buyer's favour, he will exercise his rights and receive the intrinsic value from the writer of the option.

For instance, if the spot price declines below INR 53600, XYZ Gold Inc. will choose not to exercise the option. In this way, his loss would be limited to the premium of INR 1050 per 10 grams.

In an alternative situation, when you expect the price to fall below the spot price in the future, you have the option to purchase put options. Buying a put option provides you with the advantage of selling at the strike price on the expiration date. Here also you have no obligation to exercise your right.

The swap contract involves an exchange of cash flows over time. Swaps are typically done between two parties. One party makes a payment to the other. This depends on whether a price is above or below a reference price. This reference price is the basis of the swap contract, and there is a mention regarding it in the contract.

Some Rules of investing/trading in the Derivatives market

Who are the participants in derivatives markets?

This investor buys an asset at a cheaper rate from one market and sells it at a higher price in another market, where the investor takes the minimum risk. This price gap is brief and narrows down quickly, and the arbitrageurs might lose the opportunity.

Hedging is minimizing risk or loss. An investor who protects his investment from unfavourable price movements is called a hedger in the market. A hedger tries to limit risk by buying put options and paying a fixed amount known as premiums.

They are the risk-takers. They take high risks, expecting higher gains in the short term. They buy stocks expecting a price rise and sell them at a high price level. This situation can make high gains for an investor, but it also has a high risk of losing money.

.jpg)

Harshad Mehta Was an Indian Stock Broker also referred to as the Big Bull of the Indian Stock Market. He is well known in the Indian Stock Market Circuit and well known for his wealth and luxurious life. He has been charged with multiple financial crimes in the 1992 securities market scam and using the money to manipulate the stock market by rigging the price of shares. It was alleged that Mr Harshad Mehta was engaged in a massive stock market manipulation financed by worthless bank receipts, which his firm Grow More Research and Asset Management brokered for “ ready-forward transactions between banks. It was considered one of the greatest stock market scams, which occurred in 1992, valued at over Rs 5000 crore by a man known as The Big Bull of the Indian Stock market, Harshad Mehta.

Harshad Mehta started his early Stock market Career as a Jobber in a stockbroking firm in the early 1980s. Over a period of 10 years, he served in various positions of increasing responsibility at a series of broking firms. He actively started trading in the stock market 1986 through his brokerage firm, Grow More Research and Asset Management. By 1990, he had risen to the position of The Big Bull of the Indian Stock market by the Media and Financial Market fraternity.

Banks in India were not allowed to invest in the stock market in the early 1990s. However, they were allowed to retain a certain ratio of their total assets in government fixed-interest bonds and securities to maintain their SLR ratio(Statutory Liquidity ratio). There was an extra clause that the average percentage bond holding over the week needs to be above the SLR ratio, but the daily percentage need not be so, which means banks would sell bonds at the earlier part of the week and would be back at the end of the week.

The broker would act as a middleman for the banks. Harshad Mehta squeezed capital through loopholes in the banking system to address this requirement of banks as a market maker pumped this money into the share market and rigged the share prices. In the early 1990s, Indian Banks were not highly efficient in securities operation and relied on stockbrokers to find a deal as a market maker. Harshad Mehta was a smart broker and he was able to find the loophole in a very short span of time. Further, he promised the banks a higher rate of interest sometimes asking money to transfer into his personal account on the pretext of buying securities from other banks. Mr. Harshad Mehta used this money from his account to buy shares in huge quantities, thereby hiking the demand for certain shares and skyrocketing the price. Some well-established companies like Cipla, ACC, Hindalco, Sterlite, and Videocon Industries sold off when the price rose dramatically. He had single-handedly operated the price of ACC from 200/per share to 9000/per share in a span of 3 months. Imagine the euphoria he created with his aura in the Indian Stock Market as The Big Bull. In one year, from 1st April 1991 to 31st March 1992, the BSE Sensex rose by a whopping 247%, a historic record in a financial year in the Indian Equity market to date as of 31st October 2020.

The most lucrative instrument used by Harshad Mehta in a big way to pump money into the share market was a Bank Receipt. Typically, the BR transaction was a ready-forward deal wherein securities were not moved back and forth. Instead, the borrower of money, e, the seller of securities, issues BR to the buyer of securities. The BR confirms the sale of securities. It also acts as a receipt for the money the selling bank receives and promises the delivery of securities to the buyer. The seller holds the securities in trust (as a novation)of the buyer. After figuring out this method, he needed banks that could issue fake BRs or BRs not backed by securities. Once the fake BRs were issued, they were passed on to other banks, and the bank, in turn, gave money to Mehta, assuming that they were lending to other banks against govt. Securities, which were not really the case as the BR were fake without being backed by security. The stock market was overheated because the buying spree from Mehta and Sensex had risen 247% in one year.

Sucheta Dalal, a young financial Journalist, got the tipoff about the fake BRs fraud. Sucheta kept digging about the amount of fake BRs used by Mehta to pump in the stock market. On 23rd April 1992, Sucheta Dalal exposed the scam of Harshad Mehta in the Times of India. Once the scam was exposed, Banks realized they were holding Brs of no value. The chairman of Vijaya Bank committed suicide as he issued fake BRs to Mehta in lieu of commission. Mr Mehta died at the age of 47, on 31st December 2001, due to cardiac arrest and left behind the biggest scam of the Indian Stock Market and created the historic bull run of all time till date and hence came to be known as “ The Big Bull of Indian Stock Market”.

These scams can wipe up your capital. You can get trapped in such events, so to develop your skills, you need to know about the Stock Market. You need to learn from the share market course in Delhi.

Some conclusions and evidence say that the activity was going on in the entire market and was used by all brokers in the stock market, and he was made a scapegoat as he used to believe in a bull run, and the rest of the brokers were against that. Due to Harshad Mehta, they have to suffer major losses. No doubt, the method used by the entire market was unethical, and after the scam exposed by Sucheta Dalal SEBI and the market, regulators made stringent rules and regulations to prevent the misuse of securities to manipulate the stock market.

After the web series Scam 1992 was released, the one name trending in India is Harshad Mehta. Now, Who Harshad Mehta is? What did he do exactly? In this article, we will explain about him in brief.

One of the biggest scams that struck India hard in 1992 by Harshad Mehta, AKA Big Bull&rdquo of India. Harshad Mehta was born in a middle-class Jain family of Gujrat in 1954 and spent his childhood in Mumbai. He completed his bachelor's in commerce from Lajpatrai College in Mumbai. Harshad tried his luck in many jobs like a diamond, accountant, etc. he found his major fortune in the Indian stock market only. After graduation, Mr. Mehta started his career as a salesman at the New India Assurance Company (NIACL). After a few years of hustle and not getting the geek, he showed his interest in the share market and joined a brokerage firm, B.Ambalal & Sons, where he worked as a jobber for the broker, P. D. Shukla. People start recognizing him as Amitabh Bachan of the Stock market as time passes. In 1984, Harshad Mehta started his brokerage firm and named it Growmore Research and Asset Management.

He actively started trading in the market in 1986, and by the year 1990, people had started joining him, and they were investing with his firm. In the mean years, he got some big shot clients like then minister Mr. P. Chidambaram. After getting a veteran in the market he started to manipulate the market, he manipulated the share price of Associated Cement Company (ACC) from Rs.200 to Rs.9000 in nearly just 3 months.

Now the question is where the scam started?

Until 1990, banks were prohibited from investing in the equity markets. They were expected to post profits and retain a certain ratio (threshold) of their assets in the government's fixed-interest Bonds. Mr. Mehta smartly brought the capital out of the banking window and pumped this money into the share market. He promised the banks a higher rate of interest than the normal ongoing. He asked them to transfer the amount into his account, under the belief of buying securities for them from other banks. At that time, a bank had to go through a broker to buy securities and forward bonds from other banks. Mehta got the idea from there only to use this money temporarily in his account to buy shares. Now, he started to boost the price of certain shares of already established companies like (ACC, Sterlite Industries, and Videocon ) when the market cruised at its best; he Eventually sold the shares and passed on a part of the proceeds to the bank and kept the rest into his pocket.

To carry out the scam, the deliveries of security and payment were made through the help of the broker only; for example, one seller handed over the security to the broker, and now the broker passes them to the buyer, and the buyer gave the cheque to the broker, now the broker made the payment to the seller. The buyer and the seller would not even know who they had traded with; the broker is going to be the only mediator between these two

Another instrument used in a big way was the Bank Receipt (BR). The confirmation of security sale is the BR; it 's like a receipt received by the selling bank. i.e. the seller of securities gave the buyer of the securities a BR. A BR promises to deliver the securities to the buyer and also states that, in the meantime, the seller holds the securities in the buyer's trust. Mehta cleverly found a bank providing him with fake BRs or BRs not backed by government securities. Too small and not very well known banks – the Bank of Karad (BOK) and the Metropolitan Co-operative Bank (MCB) – came in handy for this purpose. Once these fake BRs were issued, once the money was invested in the share market and was sold in profits, he returned the money to the banks.

This was all the tricks MR. Mehta was using it to boost the market, and people started calling him the Big Bull of Dalal Street; this all continued until Sucheta Dalal showed her interest in it.

Sucheta Dallas was a Young enthusiastic financial journalist, she got the tip about the SBI BR frauds. Sachet kept digging into this and found all the scams of Harshad Mehta.

On 23rd April 1992, journalist Sucheta Dalal exposed the illegal ways of Harshad Mehta in the Times of India about how Mr Mehta was using bank money in the share market.

Just after the article, Banks realizes they were holding the BRs of no value. The chairman of Vijaya Bank committed suicide after the scam exposure came out; he was found guilty of having issued checks to Mehta and knew that he would lose all the reputation he had earned in the market.

One late night under custody in Thane prison, MR. Harshad Mehta. He complained of chest pain and was admitted to the Thane Civil Hospital. He died with the following pain, at the age of 47, on 31st December 2001, he left behind the biggest scam of the Indian finance history.

To keep yourself away from these scams, you need to upgrade yourself so that you can be safe in the Stock Market, and for that, you need to join share trading course in Delhi to learn about the Stock Market

This man was Harshad Mehta from a basic middle-class family who dreamed of a big house and dived into the ocean of the finance market and brought the tornado into that ocean. People built their fortune with Mr Mehta, but in the end, he was the culprit and journalist Sucheta Dalal brought to light his scams of more than Rs 4000 crore.

.png)

Industry Analysis in Stock market

Michael Porter’s Five Force Model for Industry Analysis

Horizontal Forces

Threat of Substitutes

The threat of New Entrants

The threat of Established Rivals

Vertical Forces:

Bargaining Power of Suppliers

Bargaining Power of Customers

Barriers to entry (threat of new entrants):

Entry barriers in an industry can be understood by following simple industry characteristics.

They would be high if:

There are lots of licensing required in the business

Patents and copyrights prevent new entrants

Huge investments in specialized assets pose a challenge

Strong Brands, strong distribution network, specialized execution capabilities, customer loyalty with existing products/services exist in the business.

Attractive Industry from the Equity shareholders’ perspective:

Low competition

High barriers to entry

Weak suppliers’ bargaining power

Weak buyers’ bargaining power

Few substitutes

Pestle Analysis

Pestle Analysis stands for Political, Economic, Socio-cultural, Technological, Legal, and Environmental Analysis for investment in the Stock Market. Some models also extend this to include Ethics and Demographics, thus modifying the acronym to STEEPLED. This analysis is done more from the perspective of a business looking to set up a unit offshore and analyzing several countries to choose from in the share market. This model primarily analyses the external environmental factors that will act as influencers for a business.

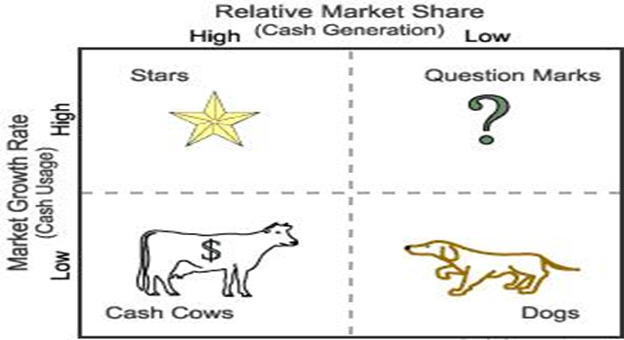

Boston Consulting Group (BCG) Analysis

Stars: These are segments in a business where the market is growing rapidly and the company has a large market share. This segment generates increasing cash for the business with time. Cera Sanitary Ware could be a good example of a “star&rdquo with a large market share, continuous growth, and significant cash generation.

Cash Cows: These are segments that require low cash infusion for investment to maintain market shares because of low growth prospects but, at the same time, steadily generate cash for the company from the established market share. Navneet Publications could be a good example of a “ cash cow in the business of books and notebooks business. The industry grows at a predictable and steady rate each year.

Question Marks Business segments in a fast-growing market with a low market share. The right strategies and investments can help the business's market share grow, but they also run the risk of consuming cash in the process of increasing market share and, in the end, not generating enough cash. Tata Nano can be considered as an example of a question mark which did not succeed, whereas Bajaj Pulsar may be considered an example of a question mark product that succeeded.

Dogs: Business segments which have slow growth rates and intensive competitive dynamics that lead to the low generation of cash are categorized as Dogs.

Key Industry Drivers for Various Sectors in share Market:

Telecom: A key parameter used to analyze this sector is the Average Revenue Per Unit (ARPU). It is calculated by total revenue divided by the number of subscribers and the higher it is, the better for the company. It must be noted that India has amongst the lowest ARPUs in the world. Other parameters like mobile penetration and spectrum costs are also important for the Telecom industry.

IT/ BPO/ KPO: The IT sector in India grew primarily due to a large, available pool of English-speaking young talent at a low cost. IT companies earned in Dollars and spent in Rupees and made huge profits. Even today, the USDINR rate, the attrition rate among employees, the concentration of revenues with selected clients, the concentration of geographies, etc. are important parameters to watch out for in IT and related sectors.

Retail: The retail sector saw a huge jump in the new millennium's first decade. Retail store formats rely on low-cost procurement of goods from manufacturers and selling it on wafer-thin margins to many people.

Banking/ NBFC/ Housing: Monetary Policy by the RBI is this sector's most significant impacting factor. NPA levels, provisioning norms, tight/loose regulatory reserve requirements all impact banks and NBFCs.

Media: Any media company depends upon content; hence, a company generating its own content will have an advantage over others. Distribution companies are almost always under pressure as there is intense competition in the sector, and content providers to media companies charge a premium. Television Rating Points (TRPs) are the most widely tracked indicator in electronic media.

COMPANY ANALYSIS

Qualitative Dimensions for Investments

What does the company do and how does it do?

Who are the customers, and why do customers buy those products and services?

How does the company serve these customers?

There are over 6000 companies listed on Indian exchanges. It is not possible to track and understand all of them. Investors should consider buying shares of a few companies they understand rather than invest in several companies they don't understand. Quoting Warren Buffet: Wide diversification is only required when investors do not understand what they are doing.

Strengths, Weaknesses, Opportunities, and Threats (SWOT) Analysis

Every business has its own strengths and weaknesses. It is good for the analysts to clearly understand and document both to have a clear picture of the situation. Similarly, the analysts can document opportunities for the business and potential risks in the form of opportunities and threats. In a way, SWOT analysis is nothing but a way of concisely documenting strengths, weaknesses, opportunities, and threats in one place. Hence, without an analysis of the company, investing can be riskier, and for better research, one needs better knowledge of the stock market. It is recommended to join stock market classes in delhi and study the different modules of the stock market, then take the step forward of investing.

Sources of Information for Analysis

Annual/Quarterly reports - Most easily available, reliable and consistent source of information

Conference Call transcripts

Investor Relation (or Company) Presentations

Management interviews on the internet

Company website

Ministry of Corporate Affairs website

Research Report from Credit Rating Companies

Research Report from various other sources – media reports

Parent Company’s annual report and website

Competitors’ website including international competitors

Print media reports on companies

Discussion with suppliers, vendors, consumers, and competitors

Start with a demonstration class.